What Is the Medicare IRMAA Surcharge?

If your income is above certain limits, you may pay more for Medicare coverage through something called IRMAA.

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an additional surcharge added to your:

- Medicare Part B premium

- Medicare Part D prescription drug coverage premium

Many people are surprised when they receive an IRMAA notice from the Social Security Administration because the increase can significantly raise monthly healthcare costs.

This guide explains:

- What IRMAA is

- Who pays it

- How Medicare determines your surcharge

- 2026 IRMAA income brackets

- Ways you may reduce or appeal IRMAA

How IRMAA Works

Most Medicare beneficiaries pay the standard monthly premium for Part B and Part D.

However, Medicare charges higher-income individuals and couples an additional premium based on income reported on their federal tax return.

Medicare typically looks at:

- Your Modified Adjusted Gross Income (MAGI)

- From your tax return filed two years earlier

For 2026 Medicare premiums, Social Security generally reviews your 2024 tax return.

What Income Counts for IRMAA?

IRMAA uses your MAGI, which includes:

- Adjusted Gross Income (AGI)

- Tax-exempt interest income

Income sources that may increase IRMAA include:

- Retirement account withdrawals

- Capital gains

- Pension income

- Social Security benefits

- Rental income

- Investment income

Even a one-time event—such as selling property or converting an IRA to a Roth IRA—can temporarily trigger higher Medicare premiums.

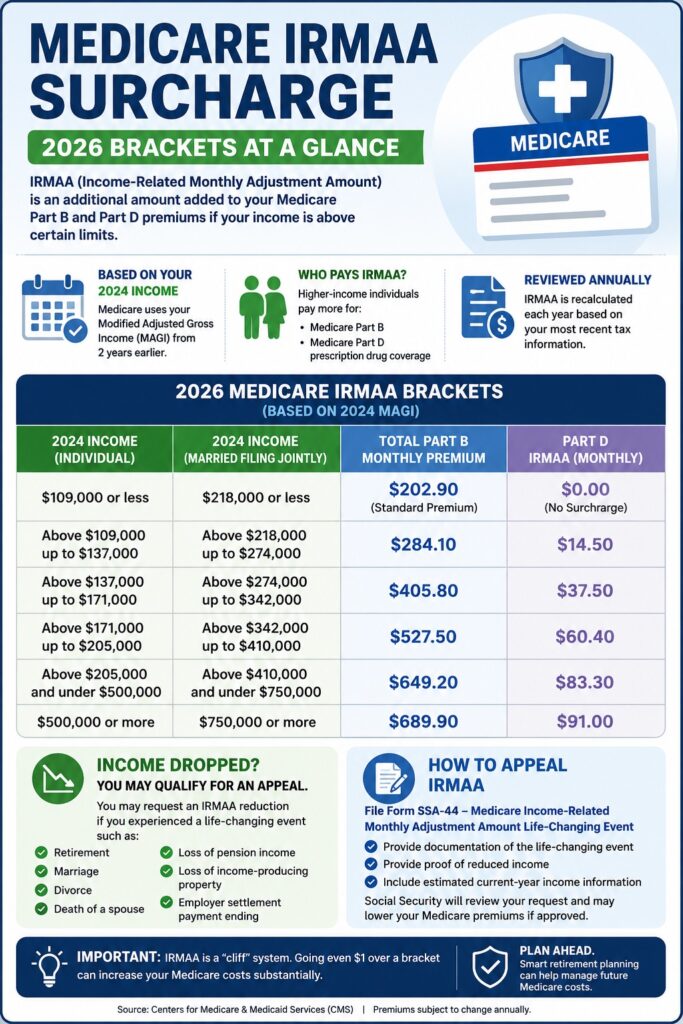

2026 Medicare IRMAA Income Brackets

| 2024 Income (Married Filing Jointly) | Total Part B Premium | Part D IRMAA | |

|---|---|---|---|

| $109,000 or less | $218,000 or less | $202.90 | $0 |

| Above $109,000 up to $137,000 | Above $218,000 up to $274,000 | $284.10 | $14.50 |

| Above $137,000 up to $171,000 | Above $274,000 up to $342,000 | $405.80 | $37.50 |

| Above $171,000 up to $205,000 | Above $342,000 up to $410,000 | $527.50 | $60.40 |

| Above $205,000 and under $500,000 | Above $410,000 and under $750,000 | $649.20 | $83.30 |

| $500,000 or more | $750,000 or more | $689.90 | $91.00 |

A few important notes:

- The standard Part B premium in 2026 is $202.90/month.

- The Part D IRMAA is added on top of your drug plan premium.

- IRMAA is a “cliff” system — going even $1 over a bracket can increase your Medicare costs substantially.

How Much Does IRMAA Increase Medicare Costs?

IRMAA can add:

- Dozens to hundreds of dollars per month to Part B premiums

- Additional monthly costs for Part D drug coverage

Because both spouses may pay separate surcharges, IRMAA can significantly affect retirement budgets.

Common Life Events That May Reduce IRMAA

Sometimes your income has dropped since the tax return Medicare used.

You may qualify for an IRMAA reduction if you experienced a major life-changing event such as:

- Retirement

- Marriage

- Divorce

- Death of a spouse

- Loss of pension income

- Loss of income-producing property

- Employer settlement payment ending

In these situations, you can request a reconsideration from Social Security.

Strategies to Help Reduce Future IRMAA Costs

While IRMAA cannot always be avoided, careful retirement planning may help reduce future surcharges.

Potential strategies include:

- Spreading out IRA withdrawals

- Managing capital gains

- Coordinating Roth conversions carefully

- Using tax-efficient withdrawal strategies

- Working with a financial advisor or tax professional

Planning ahead is especially important before age 63 because Medicare uses income from two years earlier.

Frequently Asked Questions About IRMAA

Is IRMAA Permanent?

No. IRMAA is recalculated annually based on your income.

If your income decreases, your surcharge may also decrease or disappear.

Does IRMAA Affect Medicare Advantage Plans?

IRMAA does not directly change your Medicare Advantage plan premium, but it still affects:

- Medicare Part B premiums

- Part D drug coverage costs

Does Social Security Automatically Notify Me About IRMAA?

Yes. If IRMAA applies to you, Social Security typically mails an official determination notice explaining:

- Your surcharge amount

- The income information used

- Your appeal rights

Final Thoughts

The Medicare IRMAA surcharge is essentially a higher premium paid by beneficiaries with higher incomes.

Because IRMAA is based on prior-year tax returns, retirement income planning can play a major role in controlling future Medicare costs.

Understanding how IRMAA works can help you:

- Avoid unexpected premium increases

- Prepare for retirement healthcare expenses

- Know when you may qualify for an appeal or reduction

If you are approaching Medicare eligibility or already enrolled, reviewing your income strategy early may help you minimize future surcharges and protect your retirement budget.

Need Help Understanding Medicare?

At Your Medicare MN, we help individuals and families across Minnesota understand Medicare enrollment rules, compare coverage options, and avoid costly mistakes.

Whether you are still working, retiring soon, or helping a spouse navigate Medicare, getting personalized guidance can make the process much simpler.

Visit Contact Us to schedule a personalized Medicare review and get answers tailored to your situation.

For official Medicare information, visit the Medicare.gov website.