Medicare & Your Job: What You Need to Know

Turning 65 doesn’t automatically mean you have to enroll in Medicare. If you’re still working — or covered under a spouse’s employer plan — you may have options that can save you money. But the rules are specific, and timing is important.

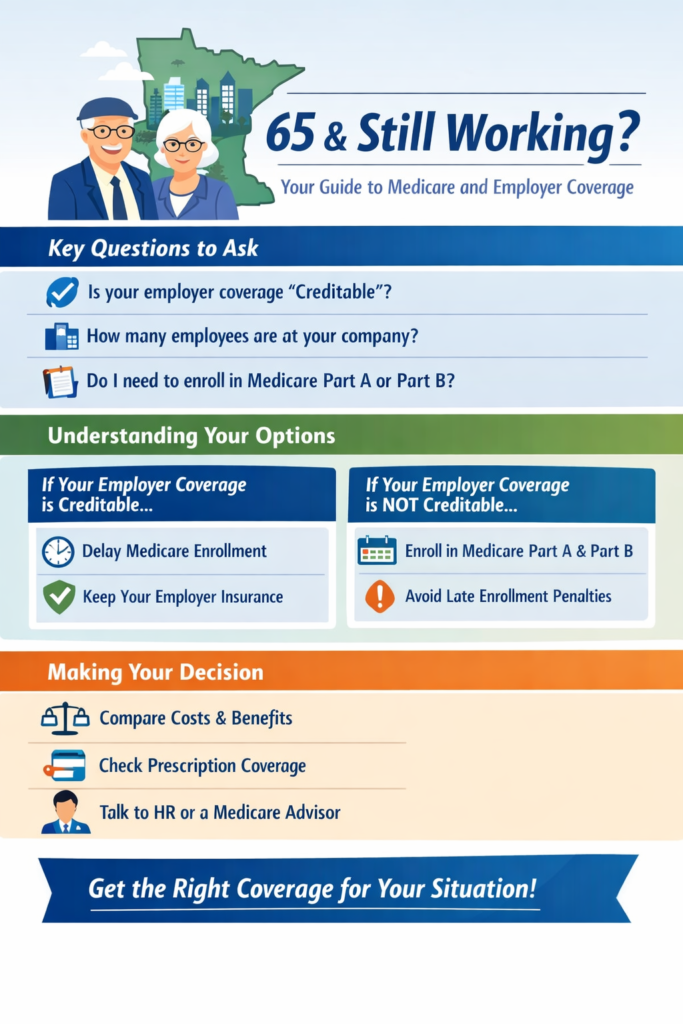

Employer Coverage vs. Medicare

Whether you need to sign up for Medicare Part B right away depends on:

- Size of your employer:

- 20+ employees – Your employer plan generally pays first. You may delay Part B without penalty.

- Fewer than 20 employees – Medicare usually becomes the primary payer.

- Creditable coverage: Your employer insurance must meet or exceed Medicare standards. If it does, you may delay Part B.

- Coverage end date: If you plan to retire or lose employer coverage soon, timing your Medicare enrollment is critical to avoid gaps and penalties.

Steps to Take if You’re Still Working

- Check your current coverage – Ask HR if your plan is “creditable” for Medicare.

- Decide on Part A and Part B – Part A is usually free, and many people enroll even while working. Part B can often be delayed without penalty if you have creditable coverage.

- Plan for your transition – If you’ll leave your job, make sure you know your Special Enrollment Period (SEP) so you can enroll in Part B or a Medicare Advantage plan without penalty.

Why Getting Help Matters

Navigating Medicare while still working can be tricky. A misstep could mean:

- Higher premiums for life

- Gaps in coverage

- Surprise medical bills

We help Minnesota residents make the right choice for their health, coverage, and budget, so you can keep working without worrying about Medicare mistakes.

How We Can Help

✔ Review your current employer coverage and deadlines

✔ Explain Medicare rules in plain language

✔ Identify your Special Enrollment Period window

✔ Compare Medicare options that work for your situation

Schedule your free consultation today and get clarity on Medicare while working.

📞 952-201-5991

📍 Serving all of Minnesota

💻 Phone and virtual appointments available

Visit Contact Us to schedule a personalized Medicare review and get answers tailored to your situation.

For official Medicare information, visit the Medicare.gov website.